In other words, Forfaiting is providing financing to exporters after receiving the confirmation that the exporter's L/C is promised to be paid by issuing bank without recourse. which means if the issuing bank refuses to pay, then the local bank(forfaiter) can't get the money from exporters.

Why companies choose Forfaiting?

- Exporters can have short-term financing without recourse.

- Exporters don't need to be worried about any risk in their business and risk shifted to the bank.

- Exporters can have immediate export rebates once Forfaiting service is done.

Characters of Forfaiting

- Financing after confirmation from issuing bank.

- Forfeiting is expensive for exporters compared with discounting/negotiation

- No limitation to the money financed for exporters.

- The time range is different, normally <= 360 days, but some long-term trade can span across to 10 years.

- A limitation to the bank performing the Forfaiting service. Normally the local negotiation bank has the ability to do Forfaiting service otherwise, it's hard for the bank to tell the veracity of the trading background or some documents. On other hands, if a bank only performing the Forfaiting service rather than negotiation service, then they can't maximize the profit.

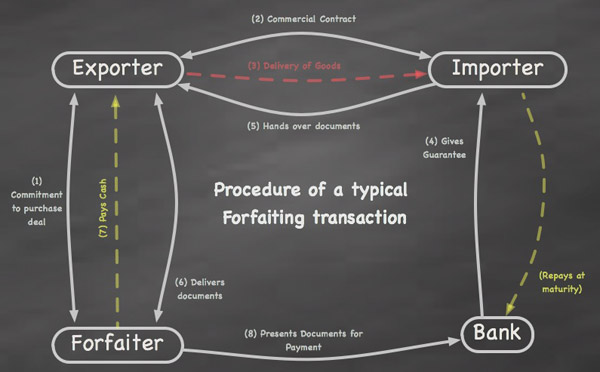

Flows

- Exporters apply for negotiation service/others in the local bank once they received L/C.

- The foreign bank(Issuing bank) gives a confirmation/promise to local banks saying they'll pay.

- The local bank tells the exporter about (2).

- Exporter applies for Forfaiting service.

- The local bank accepts the application and signs the contract, then gives the money/finance to the exporter after deducting correspond expense + interest.

- The foreign bank pays the money stipulated on L/C to the local bank(forfaiter) as time goes.

- The local bank receives the money and auto-deduct the financing cost from the exporter and closes the Forfaiting deal.

Different Forfaitings

- Direct buyout. The local bank buyout all the account receivables under the L/C provided by the exporter. Then all the profit is gained without sharing any proportion with other banks. In this case, it means the foreign bank has a good reputation where The country it's in and the economy the country has is stable. So local bank chooses to buy all.

- Indirect buyout(Risk participation). Bank A is doing Forfaiting with the exporter and have account receivables. Then Bank A sells this Forfaiting/account receivables to Bank B in a secondary market under his own concern(maybe afterward he thinks it has a risk). So Bank B is under an indirect buyout or it's normally called risk participation. Risk participation normally has 2 kinds: Funded and Unfunded.

Funded Risk Participation

Bank B buy the Forfaiting/account receivables and pay the money immediately to bank A. From that time on, It's none of the business of Bank A anymore. All the risk or benefit shift to Bank B.

Unfunded Risk Participation

Bank B buy the Forfaiting/account receivables and not pay the money to bank A. But compensate bank A once foreign Bank refusing to pay or under bankruptcy.

Example: Bank A is primary forfeiter giving Exporter C forfeiting USD 18800.00. Afterward, Bank A thinks this business has a big risk and negotiate with Bank B (secondary forfeiter) to do Unfunded Risk Participation to sell receivables. Bank B has a good relationship with the foreign issuing bank and thinks it's under control. So he agrees. Bank B doesn't need to pay. Bank A gives money to Exporter C as normal. If in future, Foreign issuing bank refuses to pay / under bankruptcy, It's none of the business of Bank A/Exporter C. As Bank A does advanced payment to C. So Bank A has the recourse to Bank B but not to Exporter C.

Normally, For the secondary forfeiter under the funded risk participation, because he must pay the money in advance, so he will normally gain a good profit (The usual quote is: Libor + some margins), but under the unfunded, he doesn't need to do advanced payment, so has low profit.

Because Forfaiting is a financing service, So you can regard it as a loan. the quote is the interest rate you gotta pay the loan. which is also the profit the bank earns.

Difference between Forfaiting and Discount

- Time Range different. Forfaiting < 10 years, Discount < = 1 Year.

- Forfaiting has no recourse, Discount has.

- The financial report is different. Discount is liability under the company balance sheet. Forfaiting is an account receivable.

- Forfaiting can help the company get tax rebates in advance, but discount can't.

- Forifating has a higher expense and interest rate compared with discount.

Forfaiting is an effective way of getting short-term finance for the exporters against their bills receivables. Today more & more exporters are catering to their instant cash requirements for business operations by applying for this kind of international trade finance. If you are a global businessman dealing in import-export services and looking for the reliable Forfaiting services, we at Emerio Banque have got you covered. This following blog will help you understand the concept better "https://www.emeriobanque.com/blogs/what-is-international-trade-finance-how-does-it-work-and-types"

ReplyDeletehttps://www.emeriobanque.com/blogs/what-is-international-trade-finance-how-does-it-work-and-types

ReplyDelete