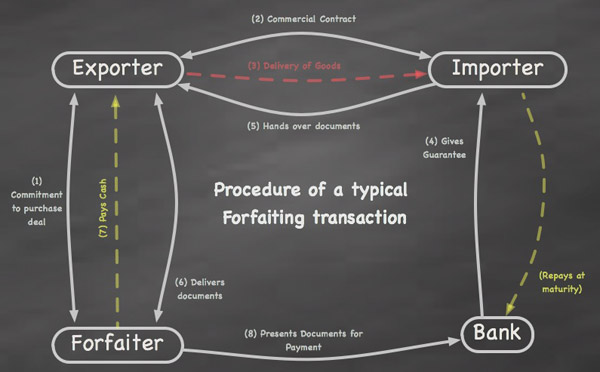

Export Trade Finacing is basically for the sellers/exportors to finance for themselves. There are quite a lot of ways for them to get money from banks, for example packing fiance/Loan, Negotiation under documentary credit, Discount, Forfeiting, Confirmed L/C, Factoring etc. Among them , Packing Finance/Loan , Silent Confirmation, Forfeiting and several others occurs when both parties' dealing based on L/C.

Basis

Packing Loan: Exportors(choosing L/C as the way of transaction settlement) can apply for a certain amount of financing before their cargo loading upto the ship to export(

Packing stage). Exportors just need to submit the L/C they received from buyer side's bank to the bank they plan to apply the loan from as a collateral to get the money.

Packing Loan initially is invented to solve the fiancing need for exportors in their packing stage. But nowadays, most of banks don't follow this. whatever reasons like : goods replenish, goods processing and other steps before the shippment of the goods . you all can appy for packing loan as long as your L/C is real!

Some Banks will need the L/C as a collateral to give the loan out. some just need to check the exportor's credit . but in Aisa, most of banks still need the L/C as a colateral.

Characteristic

- Exportor can only use this money to designated items. they can't use it to other investment e.g fix asset investment etc.

- Bank will keep the original L/C as collateral to make sure the applier/Exporter do the presentation of documents in this bank so as to monitor all the way how's the L/C's status.

- Packing loan's time is short. <= 36 days.

- With recourse. If exportor can't get the money from importor, bank have the right to deduct principal + interest from the exportor's other account directly

Documents Needed

- Company basic liscences and certificates . e.g: tax register liscense. business entity information...

- Fill the application form that bank provides

- Provide the company financial health evidence e.g Audited P/L, Balance sheet...

- Original L/C and contracts

- Deposit

- Others

Interest Calculation

Loan Amount:

The Amount Exportor can get(Loan Amount) = L/C Amount * Margin

The Margin is set by the bank internally.normally the higher the credit of the exportor , the higher the margin will be . normally the margin is between 70%~90%,if A L/C is 1M , then normally the company can get 700K ~90K loan amount.

Annual Interest Rate:

Annual Interest rate is calculated based on different currencies .If Loan is USD, then use USD loan interest rate , if Loan is YEN, then use Yen loan interest rate.The interest rate is synced with the central bank. Normally , The bank will choose the latest loan expiry date to let the exportor pay back the principal and interest rate together.

Foreign Currency Financing normally is based on the

Inter-Bank Offer Rate (e.g: USD : Libor, YEN: Tibor) + Margin. For exmaple, For USD, Normally the

interest rate = Libor + 0.5%~1.5%.For some companies with good credit/reputation, The bank also can only charge Libor + 0.25% as the interest.

Take the data from 28th April 2006 as a example, 12 month Libor is 5.28%, So the bank can choose the interest rate between

5.53% (5.28% + 0.25%) ~ 6.78% (5.28% + 1.50%) to charge the exportor.

Of course , there're still some banks taking the approach of 20th century, No matter how long the loan they give, alwayse use 1 year walking capital interest rate to charge even though some are less than 1 year. For Example, 2006 April, 1 year foreign currency walking capital loan rate is 6.75%, then the annual interest rate the bank charge the exportor apply for the packing loan is 6.75% as well.

Libor : Currently is regaded as a basis rate of floating rate(USD), It is regarded as a

financing cost of ( borrow money and re-lend out). The 3 month and 6 Month Libor are most universally used.

Packing Loan giving days:

Packing Loan giving days = the day to apply for packing loan ~ the latest shipment date stipulated in L/C + 30 Days

For Example , The L/C beneficiary(Exportor) apply for a packing loan on 10/11/2013, The Lastest shipment date in L/C is 31/12/2013. So The Packing Loan giving days are (10/11 ~ 31/12) +30 days = 81days. That is between 10/11/2013 ~ 31/01/2004. Normally It is less than 1 year. So The bank will give the money to the exportor gradually within this period.

For Companies to consider

- Company should maintain a good credit and no bad records in the bank.

- make sure the issuing bank's country economy stability and no political risk, so the payment can be done successfully.

- Read the L/C clause carefully.The more complex the clause , the harder the beneficiary to follow.

- Make sure the L/C is irrevocable L/C as the bank only can give packing loan based on this.

- Choose the correct currency to save the cost.

Exportor can choose domestic currency or froeign currency from bank. company may need to consider the national foreign currency control policy. In Recent years, In China , The foreign Currency loan interest rate is lower than the RMB loan interest rate. So companies may consider to choose foreign currency as loan currency . when using RMB, they will convert the foreign currency into RMB to save the cost.

For example, If exportor need 1M RMB to buy raw material and apply for the packing loan.the company can choose foreign currency packing loand or RMB packing loan. In 2004, RMB loan interest rate is 4.65% and USD loan interest rate 2.98%. Exchange rate at that time is USD100 = CNY826.46 .If choose foreign currency packing loan for 90 days, the interest exportor need to pay :

$ 1M * 2.98% * 90/360 = $ 7649

$ 7649 = 61.7 K (RMB)

If choose RMB packing loan , company need to pay interest:

$ 1M * 8.264 * 4.65% * 90/360 = 96.1K (RMB)

So ,Choose USD packing loan is better.

For Banks to consider

- Understand application company's credit and capital situation

- verify the L/C(By SWIFT)

- Understand Issuing Bank's credit and rate(Moody's Finth Rating).

- verify the clause of L/C

- Control the date of giving loan

- make sure the Risk Index and credit limit

Credit Limit(trade finance) = walking capital loan amount * (1 / risk index)

For example:

If bank of china gives the company A 1M USD loan limit, then A can transfer this 1M loan limit into guarantee limit:

guarantee limit = 1M USD * (1/0.25) = 4M USD

Any Question About this Product Can leave your comments below.