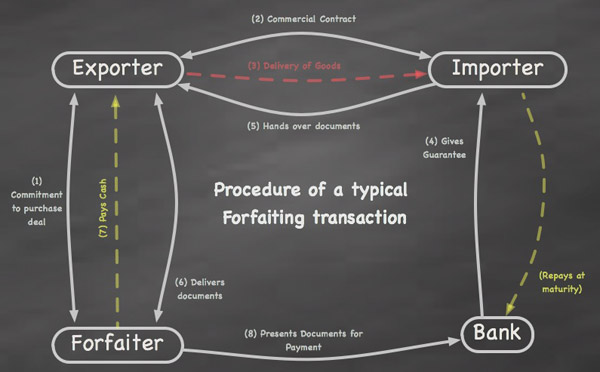

Factors (Banks) buy in those account receivables (invoices) from exporting firms and then do sales control, bad debt guarantee, trade finance etc. This comprehensive post-sale service is called

Factoring. Exporters can request the bank to provide full services or partial services.

Banks normally must join (

Factors Chain International: FCI) to be qualified as a factor. FCI members themselves will do a paperless transaction via

EDIFactoring (a digital system).

The content of Factoring service

- Maintenance of the sales ledger

Each invoice, each transaction between exports and importers will be properly managed by banks' powerful accounting system. so exporter can anytime download and check online those properly managed accounts. No need to worry about that financial management stuff. This reduces a certain cost of exporters.

Collecting money from the buyers is a somewhat hard job for most companies. Bank has a powerful debt collecting technic to deal with those importers/importers' banks. This can help exporters a lot.

Banks will use its own network to know the counterparty's credit risk. This can evaluate the debtors' credit on the fly anytime, which reduce the risk for exporters.

- Full Protection from Bad debt

Exporters finishing the goods delivery or other services normally can submit the invoice(account receivables) to factors to get > 90% finance of invoice amount.

Varieties of Factoring service

- Recoursed Factoring vs Non-recourse factoring

- Maturity Factoring vs Financed Factoring

In Maturity factoring, banks will make a specific date in future to pay the exporters in a shot. That date is called maturity date. In Financed Factoring, once the bank receives the money, it will transfer the <= 90% amount received into exporter's account. the leftover 10% will be paid in the end.

- Disclosed Factoring vs Undisclosed Factoring

In Disclosed Factoring, Suppliers/Exporters must inform all his clients in the paper to let them pay directly to the factor. In the undisclosed factoring, factor's involvement is a secret for the clients, they still pay the money to the exporter, the cost incurred will on the exporter side.

Why exporters/suppliers choose Factoring?

- Increase exporter's sales, As exporter choose factoring service, he can provide more flexible payment methods like (Open Account), (Document against Acceptance) which makes the sales easier.

- Reduce risk, factor helps exporter do all the background research, debt chasing, account management and other services like a babysitter.

- Reduce cost.

- Convenience. Avoid the inconvenience of normal L/C proceduces.

Why Buyers/Importers like Factoring as well?

- Reduce importing cost. No L/C needed. so don't need to submit those documents and pay some fees

- Goods quality is guaranteed. Factor has the control.

Procedures of Factoring service

1) Exporter signs export contract with an importer and agree on the payment type as D/A or O/A under Factoring. Then exporters go to

Export factors to apply and also need to request to verify the credit line in the factor side.

2) Export Factor(Exporter's Bank) submits all the relevant information to the Import Factor(Importer's Bank) and request to check & rectify the Factoring amount.

3) Import Factor does some background research and evaluation to the importer and decides whether to give this Factoring amount. (< 2 weeks)

4) Import Factor after initial verification will inform export factor the credit line and factoring amount of importer.

5)Export Factor will inform the exporter the verified factoring amount in written form and seek for agreement from the exporter. once exporter agrees on this amount, exporter factor will sign the factoring agreement with exporter formally.

6) Exporters ship the goods accordingly and transfer the creditor's right to the export factor signing <

The Agreement on Transfer of Creditor’s Rights > with the factor, and send <

Intrudoctory letter> to he Importer telling him that the creditor's right has been shifted to the factor and please pay as the factors' indication.

7) Export Factor will submit all the invoices/documents provided by the exporter to Import Factor, and at this stage, the exporter can ask for financing(<= 90% of invoice amount) from export factor.

8) Import factor will transfer the invoices/documents to the importer.

9) The importer will pay to import factor.

10) Import factor deducting some factoring fee will transfer the remainings to export factor.

11) Export factor deducting some factoring fees and financing amount requested from exporter before will transfer the remainings to exporter's account.

Factoring fee = Factoring rate * Factoring amount, Rate is (0.5% ~ 2%).

Trade financing interest calculation is similar to the rest, no need to discuss anymore.